EU illegal state aid case against Apple in Ireland

On 29 August 2016, after a two-year investigation, Margrethe Vestager of the European Commission announced: "Ireland granted illegal tax benefits to Apple".[1] The Commission ordered Apple to pay €13 billion, plus interest, in unpaid Irish taxes from 2004–14 to the Irish state.[2] It was the largest corporate tax "fine" (in fact a recovery order, technically not a fine) in history.[3] On 7 September 2016, the Irish State secured a majority in Dáil Éireann to reject payment of the back-taxes,[4] which including penalties could reach €20 billion,[5] or 10% of 2014 Irish GDP.[lower-alpha 1] In November 2016, the Irish government formally appealed the ruling, claiming there was no violation of Irish tax law,[6][7] and that the commission's action was "an intrusion into Irish sovereignty", as national tax policy is excluded from EU treaties.[8] In November 2016, Apple CEO Tim Cook, announced Apple would appeal,[9] and in September 2018, Apple lodged €13 billion to an escrow account, pending appeal.[10] In July 2020, the European General Court struck down EU tax decision as illegal, ruling in favor of Apple.

| Ireland v Commission | |

|---|---|

| Decided 15 July 2020 | |

| Case number | T‑778/16, T‑892/16 |

| ECLI | ECLI:EU:T:2020:338 |

| Chamber | Seventh |

| Language of Proceedings | English |

| Judge-Rapporteur Vesna Tomljenović | |

| President Marc van der Woude | |

Judges

| |

| Keywords | |

| State aid — Aid implemented by Ireland — Decision declaring the aid incompatible with the internal market and unlawful and ordering recovery of the aid — Advance tax decisions (tax rulings) — Selective tax advantages — Arm’s length principle | |

| Taxation |

|---|

|

| An aspect of fiscal policy |

.jpg.webp)

The issue was Apple's variation of the 'double Irish' tax system, which, from 2004 to 2014, Apple used to shield €110.8 billion[5][12] of non–US profits from tax.[13] Apple did not use the standard two separate Irish companies, as Google and other Irish-based US multinationals employ with their 'double Irish' tax systems, but instead received two rulings from the Irish Revenue Commissioners (in 1991, and again updated in 2007), that it could use a single Irish company, split into "two branches". These were private rulings to Apple, not given to other Irish-based US multinationals, and thus charged as illegal Irish state aid by the commission.[11]

On 9 January 2015, Apple informed the Commission[lower-alpha 2] that it closed its hybrid–Double Irish, base erosion and profit shifting ("BEPS") tool.[14] In Q1 2015, Apple restructured into a new Irish BEPS tool called the Capital Allowances for Intangible Assets (CAIA) tool,[12][15] also called the "Green Jersey". Apple's Q1 2015 restructuring required a 12 July 2016 restatement of Irish 2015 GDP, which increased it by 26.3 percent (later revised to 34.4 percent); the restatement was called "leprechaun economics", and led to new EU inquiries in 2017,[16][17] and accusations in June 2018, that Ireland was the world's largest tax haven.[18]

Ireland's rejection of the EU Commission's "windfall" in back-taxes surprised some.[19] However, in § Understanding Irish decision, US-controlled multinationals are 25 of Ireland's top 50 companies; pay over 80% of all Irish corporate taxes (circa €8 billion per annum);[20] directly employ 10 percent of the Irish labour force which rises to 23 percent when public sector, agri and finance jobs are excluded [21][22] (and indirectly pay half of all Irish salary taxes); and are 57 percent of all non-farm OECD value-add in the Irish economy. In June 2018, the American–Ireland Chamber of Commerce estimated the value of US investment in Ireland was €334 billion, exceeding Irish GDP (€291 billion in 2016).[23]

On 15 July 2020, the European General Court ruled that the Commission "did not succeed in showing to the requisite legal standard" that Apple had received tax advantages from Ireland, and ruled in favour of Apple.[24]

On 25 Sept 2020, Executive Vice-President Margrethe Vestager said they would appeal the decision before the European Court of Justice as the Commission believes the General Court has made a number of errors of law. [25]

Background

.jpg.webp)

History of Apple in Ireland

On 23 December 1980, Apple opened production facilities in Holyhill, Cork.[26][27] By 1990, the number of jobs had grown from 700 jobs to 1000 permanent jobs, as well as 500 sub-contractors.[28] Interview excerpts, published by European Commission, found that this information was used in the way of background information by a tax adviser representing Apple during meetings with Apple in 1990.[29]

By November 2016, Apple employed 6,000 people in Ireland, almost all of whom were in the Apple Hollyhill Cork plant. The Cork plant is Apple's only self-operated manufacturing plant in the world (Apple otherwise always contracts to third party manufacturers). Holyhill is considered a low-technology facility, building iMacs to order by hand, and in this regard is more akin to a global logistics hub for Apple (albeit located on the island of Ireland). No research is carried out in the facility.[30] Unusually for a plant, over 700 of the 6,000 employees work from home (the largest remote percentage of any Irish technology company).[31][32]

Apple's unusual Cork plant should be seen in the context of the job thresholds Ireland places on US multinationals making use of the main Irish BEPS tools, discussed here, which provide effective Irish tax rates of 0–2.5%, but require specific employment quotas; and give more "substance" to the BEPS tool.

Apple's Irish structure

.png.webp)

In 2014, Apple's Irish structure consisted of two subsidiaries; Apple Operations Ireland ("AOI") an Irish-registered holding company which acts as an internal financing company. AOI claimed tax residence in Bermuda and thus, is not an Irish tax resident (the use of such a company in corporate tax structuring is sometimes referred to as a "Bermuda Black Hole").[33] The EU Commission State Aid recovery order does not pertain to AOI.

Apple Sales International ("ASI"), on the other hand, is the focus of the EU Commission's recovery order(and was the focus of 2013 Senate Investigation). ASI is an Irish-registered subsidiary of Apple Operations Europe ("AOE").[34] Both AOE and ASI are parties to an Irish advanced pricing agreement which took place in 1991.[35] This agreement was updated in 2007.[36] ASI is the vehicle through which Apple routed €110.8 billion in non–US profits from 2004 to 2014, inclusive.[12]

| Year |

ASI Profit Shifted (USD m) |

Average €/$ rate |

ASI Profit Shifted (EUR m) |

Irish Corp. Tax Rate |

Irish Corp. Tax Avoided (EUR m) |

|---|---|---|---|---|---|

| 2004 | 268 | .805 | 216 | 12.5% | 27 |

| 2005 | 725 | .804 | 583 | 12.5% | 73 |

| 2006 | 1,180 | .797 | 940 | 12.5% | 117 |

| 2007 | 1,844 | .731 | 1,347 | 12.5% | 168 |

| 2008 | 3,127 | .683 | 2,136 | 12.5% | 267 |

| 2009 | 4,003 | .719 | 2,878 | 12.5% | 360 |

| 2010 | 12,095 | .755 | 9,128 | 12.5% | 1,141 |

| 2011 | 21,855 | .719 | 15,709 | 12.5% | 1,964 |

| 2012 | 35,877 | .778 | 27,915 | 12.5% | 3,489 |

| 2013 | 32,099 | .753 | 24,176 | 12.5% | 3,022 |

| 2014 | 34,229 | .754 | 25,793 | 12.5% | 3,224 |

| Total | 147,304 | 110,821 | 13,853 |

ASI's 2014 structure was an adaptation of a Double Irish scheme, an Irish IP–based BEPS tool used by many US multinationals. Apple did not follow the traditional Double Irish structure of using two separate Irish companies. Instead, Apple used two separate "branches" inside one single company, namely ASI.[11] It is this "branch structure" the EU Commission alleged was illegal State aid, as it was not offered to other multinationals in Ireland, which had used the traditional "two separate companies" version of the Double Irish BEPS tool.

Under the Double Irish structure, one Irish subsidiary (IRL1) is an Irish registered company selling products to non–US locations from Ireland. The other Irish subsidiary (IRL2) is "registered" in Ireland, but "managed and controlled" from a tax haven such as Bermuda. The Irish tax code considers IRL2 a Bermuda company (used the "managed and controlled" test), but the US tax code considers IRL2 an Irish company (uses the registration test). Neither taxes it. Apple's subsidiary, ASI, behaved like it was IRL2, it was "managed and controlled" via ASI Board meetings in Bermuda, so Irish Revenue did not tax it. But ASI also did all the functions of IRL1, making circa €110.8 billion[5] of profits from non–US sales. The EU Commission contest IRL1's actions made ASI Irish, and the functions of IRL1 over-rode the Bermuda Board meetings in deciding the "managed and controlled" test. The commission had not brought any cases against US multinationals using the standard double two separate companies Irish BEPS tool.

Apple's unique ASI structure, is believed to be the reason why Apple never had an Apple retail store in the Republic of Ireland (it even has one in smaller Belfast).[37]

EU investigation

Opening (2014)

In May 2013, Apple's tax practices were examined by a US bipartisan investigation of the Senate Permanent Subcommittee on Investigation.[39] The investigation aimed to examine whether Apple used offshore structures, in conjunction with arrangements, to shift profits from the US to Ireland.[40] Senators Carl Levin and John McCain drew light on what they referred to as a special tax arrangement between Apple and Ireland which allowed Apple to pay a corporate tax rate of less than 2%.[41][42][43][44]

In June 2014, an investigation was opened by the European Commissioner for Competition on behalf of the EU Commission (SA 38373).[45] The Ireland case was opened in conjunction with two other similar cases; involving Starbucks (Netherlands) and Fiat (Luxembourg). A small team of four people conducted the investigation by the European Commission.[46] The Commissioners noted concerns that discretion in transfer pricing rules had been used to give Apple selective advantage. They believed that this violated Article 107(1) of the Treaty on the Functioning of the European Union (TFEU).[47] Article 107(1) states that aid granted by member states cannot threaten to distort competition.[48] They examined Irish tax rulings from 1991 and 2007 by the Irish Office of the Revenue Commissioners. The Commission referred to taxable profit allocated to the Irish branches of AOE and ASI. The Commission claimed the pricing arrangement between Apple and Ireland was not supported by an economic assessment and was in part supported by employment considerations.[49]

Finding (2016)

.jpg.webp)

On 30 August 2016, the Commission released a 4-page press release describing its decision and rationale.[1] The EU Commission's full 130-page report on its State aid findings, including partially redacted information on Apple's Irish business (e.g. profits, employees, Board minutes etc.), was released on 30 August 2016.[2]

According to the commission, the tax arrangement between Ireland and Apple qualifies as state aid as it meets the European Union's four criteria:[51]

- There has been an intervention by the State

- This intervention gives the benefactor a competitive advantage on a selective basis

- As a result, competition has been or may be distorted

- The intervention is likely to affect trade between the Member States

Member States cannot give tax benefits to selected companies – this is illegal under EU state aid rules. The Commission's investigation concluded that Ireland granted illegal tax benefits to Apple, which enabled it to pay substantially less tax than other businesses over many years. In fact, this selective treatment allowed Apple to pay an effective corporate tax rate of 1 percent on its European profits in 2003 down to 0.005 percent in 2014.

— Margrethe Vestager, "State aid: Ireland gave illegal tax benefits to Apple worth up to €13 billion", 30 August 2016.[1]

The 30 August 2016 press briefing summarised the following findings from the main report:[1]

- The taxable profits of Apple Sales International and Apple Operations Europe in Ireland are determined by a tax ruling granted by Ireland in 1991, which in 2007 was replaced by a similar second tax ruling. This tax ruling was terminated when [ASI] and [AOE] changed their structures in 2015;

- Two tax rulings issued by Ireland to Apple have substantially and artificially lowered the tax paid by Apple in Ireland since 1991;

- These rulings endorsed a way to establish the taxable profits for two Irish companies of the Apple group [..] which did not correspond to economic reality;

- As a result of the allocation method endorsed in the tax rulings, Apple only paid an effective corporate tax rate that declined from 1% in 2003 to 0.005% in 2014.

The 30 August 2016 press briefing made the following statements regarding the financial implications:[1]

- The Commission can order recovery of illegal state aid for a ten-year period preceding the Commission's first request for information in 2013;

- Ireland must now recover the unpaid taxes in Ireland from Apple for the years 2003 to 2014 of up to €13 billion, plus interest [and normal penalties].

Recovery order (2016)

The recovery order for €13 billion was an estimate subject to final ASI accounts. It covers the period 2004 to 2014 inclusive, as the commission is permitted to order a full recovery within a 10-year period from the start of an investigation. The January 2018 updated estimate of the recovery order had risen to €13.85 billion.[12] The Commission recovery order is simply the estimated profits of, mainly, ASI applied, at the prevailing Irish corporate tax rate of 12.5% (see Table 1 above; and full EU Commission report).[2][5] In addition, Apple will also owe interest penalties at the Irish Revenue penalty rate (was 8% in 2016), which would total circa €6 billion, giving a total recovery order of circa €20 billion.[5]

A fallback position of the EU Commission's State aid case is that if ASI is not an Irish company, then it was a "stateless" company (given it was "legally" registered in Ireland), and Apple has been remitting royalty payments from EU–28 countries to a company in a jurisdiction with no EU tax treaty. Apple would, therefore, owe back-taxes to each individual EU country, from which these royalties were paid (and not to Ireland). As all other EU countries have corporation tax rates materially in excess of Ireland's 12.5% corporation tax rate, the total Apple effective taxes owned, in this scenario, would be materially in excess of €13 billion. Margrethe Vestager appealed to individual EU taxing authorities to assess this aspect of Apple's State aid case for themselves, on a case-by-case basis.[54]

In fact, the tax treatment in Ireland enabled Apple to avoid taxation on almost all profits generated by sales of Apple products in the entire EU Single Market. This is due to Apple's decision to record all sales in Ireland rather than in the countries where the products were sold. This structure is however outside the remit of EU state aid control. If other countries were to require Apple to pay more tax on profits of the two companies over the same period under their national taxation rules, this would reduce the amount to be recovered by Ireland.

— Margrethe Vestager, "State aid: Ireland gave illegal tax benefits to Apple worth up to €13 billion", 30 August 2016.[1]

Appeal (2016–2020)

In November 2016, in a letter to the Apple community in Europe, Tim Cook said the company would appeal.[9] In the immediate aftermath of the commission's 29 August 2016 ruling, Ireland's finance minister Michael Noonan stated that Ireland would be appealing the decision, subject to cabinet approval.[55] On 2 September 2016, the Irish cabinet voted to approve the appeal.[56] The minority Fine Gael–led government also had to secure a general Dáil Éireann vote on the matter, which it did on 7 September, by a majority of 93 to 36, securing the support of the other main Irish political party, Fianna Fáil.[4][57] In November 2016, the Irish government also formally notified the EU Commission it would appeal and reject any claim to the €13 billion "windfall".

The appeal will firstly be heard in the EU's General Court, with any further appeal being taken to the EU's highest court; the European Court of Justice.[58][59]

In August 2018, it was reported that the appeal would begin before the end of 2018, but could take over 5 years,[60] and that Apple had begun to lodge the €13 billion into an escrow account during Q2 2018.[10] On 18 September 2018, it was reported that Apple had lodged the €13 billion, plus another €1.3 billion,[lower-alpha 3] into the Irish State's escrow account.[61][62] In October 2018, the commission announced that it would drop its legal action against Ireland for failure to recover the amount owed by the deadline laid down in the Commission decision (the deadline was 3 January 2017).[63]

In May 2019, the Irish Public Accounts Committee was told by officials from the Department of Finance that defending the Apple case (i.e. to prevent the payment of the fine to Ireland), had cost the Irish state €7.1 million in mostly legal fees, and that the final case may take a decade to reach a final verdict.[64][65]

On 15 July 2020, the European General Court (EGC) ruled that the Commission "did not succeed in showing to the requisite legal standard" that Apple had received tax advantages from Ireland, and ruled in favour of Apple.[24] The EGC noted that their ruling[66] can be appealed to the Court of Justice of the European Union, which could take several more years; Apple funds would remain in escrow until such an appeal was concluded.[24]

In September 2020, the European Commission appealed against the court ruling by the European General Court that said Apple did not have to pay €13 billion because the Commission considered that in its judgment the General Court has made a number of errors of law.[67]

Further controversy

.png.webp)

.png.webp)

The EU Commission's findings cover the period from 2004 to end 2014, and its report notes that Apple had informed it at the start of 2015 that the controversial hybrid–Double Irish BEPS tool, ASI, had been closed down; which enabled the commission to complete its State aid report, and finalise the recovery order of €13 billion.[2]

In January 2018, economist Seamus Coffey, Chairman of the State's Irish Fiscal Advisory Council,[68] and author of the State's 2017 Review of Ireland's Corporation Tax Code,[69][70] showed Apple restructured ASI into another Irish IP–based BEPS tool, the Capital Allowances for Intangible Assets ("CAIA"), in Q1 2015.[12][17][15]

It is specifically prohibited under Ireland's own corporation tax code (Section 291A(c) of the Irish Taxes and Consolation Act 1997) to use the CAIA BEPS scheme for reasons that are not "commercial bona fide reasons" and in particular for schemes where the main purpose is "... the avoidance of, or reduction in, liability to tax".[71][72][73] Given that the CAIA scheme is a deliberate IP–based BEPS tool, it is Ireland tripping over itself trying to maintain OECD-compliance.

The November 2017 Paradise Papers leaks revealed that Apple and its lawyers, Applebys, were looking for a replacement for the ASI structure in 2014. They considered a number of tax havens (especially Jersey). Some of the disclosed documents left little doubt as to the key drivers of Apple's decision making.[74][75][76][77]

If the Irish Revenue waived Section 291A(c) for Apple's 2015 restructuring, it could result in a further EU Commission State Aid investigation.

In January 2018, in a series of articles in The Sunday Business Post, Mr Coffey estimated that since the 2015 restructuring, Apple has avoided Irish corporate taxes totalling circa at €2.5–3bn per annum (at the 12.5% rate).[12][78] Mr Coffey calculated the potential second EU Apple State aid recovery order for the 2015–2018 (inclusive) period, would therefore reach circa €10bn, excluding any interest penalties.[17][79]

The Irish financial media further noted that the then Finance Minister Michael Noonan, had increased the tax relief threshold for the Irish CAIA scheme from 80% to 100% in the 2015 budget (i.e. reduce the effective Irish corporate tax rate from 2.5% to 0%). This was changed back in the subsequent 2017 budget by Finance Minister Paschal Donohoe, however firms which had started their Irish CAIA scheme in 2015 (like Apple), were allowed to stay at the 100% relief level for the duration of their scheme,[80][81] which can, under certain conditions, be extended indefinitely.[73]

In November 2017, it was reported that the EU Commission had already asked for details on Apple's Irish structure post its January 2015 ruling.[16]

The April 2017 release of Irish corporation tax returns showed an equivalent "leprechaun economics"–like jump. It led some to wonder whether Apple decided, given the exposure of its CAIA BEPS tool, and the controversy of "leprechaun economics", to "still pay tax in Ireland".

In February 2019, Sinn Féin MEP Matt Carthy discussed Apple's use of the CAIA Irish BEPS tool with Margrethe Vestager.[82]

Irish decision

After 29 August 2016 ruling, the EU Commission followed up on 31 August to counter statements from the Irish Government that Ireland would have to use the proceeds of any Apple recovery to pay down public sector debt (in line with agreed EU budgetary rules), and to clarify that Ireland could allocate the money in whichever way the Irish Government lawfully saw fit.[84] Regardless however, on 7 September, the Irish minority Government, with material opposition support,[85] rejected the EU Commission's ruling on Apple, and the payment of €13 billion, plus penalties, to the Irish State.[4][57]

Economic model

American multinationals play a substantial role in Ireland's economy, attracted by Ireland's BEPS tools, that shield their non–US profits from the historical US "worldwide" corporate tax system. In contrast, multinationals from countries with "territorial" tax systems, by far the most common corporate tax system in the world, don't need to use corporate–tax havens such as Ireland, as their foreign income is taxed at much lower rates.[86]

For example, in 2016–17, US–controlled multinationals in Ireland:

- Directly employed one–quarter of the Irish private sector workforce;[22]

- Created "higher-value" jobs at an average wage of €85k (€17.9 billion wage roll for 210,443 staff) vs. Irish domestic industrial wage of €35k;[87]

- Paid €28.3 billion in 2016 in taxes (€5.5 billion), wages (€17.9 billion on 210,443 staff) and capital spending (€4.9 billion);[21][87]

- Paid 80 percent of Irish corporation and business taxes, which totalled just over €8 billion;[20]

- Paid circa 50 percent of Irish salary taxes (due to higher paying jobs), 50 percent of Irish VAT, and 92 percent of Irish customs and excise duties;

(this was claimed by a leading Irish tax expert (and Past President of the Irish Tax Institute), but is not fully verifiable)[88] - Created 57 percent of private sector non-farm value-add (40% of value-add in Irish services and 80% of value-add in Irish manufacturing);[22][89]

- Made up 25 of the top 50 Irish companies, by 2017 turnover (see Table 2, below); the only non–U.S/non–Irish other companies are UK companies which either sell into Ireland, like Tesco, or date from pre–2009, when the UK reformed its corporate tax system to a "territorial" regime.[90]

- American–Ireland Chamber of Commerce estimated the value of US investment in Ireland in 2018 was €334 billion, exceeding Irish GDP (€291 billion in 2016).[23]

| Rank (By Revenue) |

Company Name[90] |

Operational Base[91] |

Sector (if non–IRL)[90] |

Inversion (if non–IRL)[92] |

Revenue (2017 €bn)[90] |

|---|---|---|---|---|---|

| 1 | Apple Ireland | United States | technology | not inversion | 119.2 |

| 2 | CRH plc | Ireland | – | – | 27.6 |

| 3 | Medtronic plc | United States | life sciences | 2015 inversion | 26.6 |

| 4 | United States | technology | not inversion | 26.3 | |

| 5 | Microsoft | United States | technology | not inversion | 18.5 |

| 6 | Eaton | United States | industrial | 2012 inversion | 16.5 |

| 7 | DCC plc | Ireland | – | – | 13.9 |

| 8 | Allergan Inc | United States | life sciences | 2013 inversion | 12.9 |

| 9 | United States | technology | not inversion | 12.6 | |

| 10 | Shire | United kingdom | life sciences | 2008 inversion | 12.4 |

| 11 | Ingersoll-Rand | United States | industrial | 2009 inversion | 11.5 |

| 12 | Dell Ireland | United States | technology | not inversion | 10.3 |

| 13 | Oracle | United States | technology | not inversion | 8.8 |

| 14 | Smurfit Kappa Group | Ireland | – | – | 8.6 |

| 15 | Ardagh Glass | Ireland | – | – | 7.6 |

| 16 | Pfizer | United States | life sciences | not inversion | 7.5 |

| 17 | Ryanair | Ireland | – | – | 6.6 |

| 18 | Kerry Group | Ireland | – | – | 6.4 |

| 19 | Merck & Co | United States | life sciences | not inversion | 6.1 |

| 20 | Sandisk | United States | technology | not inversion | 5.6 |

| 21 | Boston Scientific | United States | life sciences | not inversion | 5.0 |

| 22 | Penneys Ireland | Ireland | – | – | 4.4 |

| 23 | Total Produce | Ireland | – | – | 4.3 |

| 24 | Perrigo | United States | life sciences | 2013 inversion | 4.1 |

| 25 | Experian | United Kingdom | technology | 2006 inversion | 3.9 |

| 26 | Musgrave Group | Ireland | – | – | 3.7 |

| 27 | Kingspan Group | Ireland | – | – | 3.7 |

| 28 | Dunnes Stores | Ireland | – | – | 3.6 |

| 29 | Mallinckrodt Pharma | United States | life sciences | 2013 inversion | 3.3 |

| 30 | ESB Group | Ireland | – | – | 3.2 |

| 31 | Alexion Pharma | United States | life sciences | not inversion | 3.2 |

| 32 | Grafton Group | Ireland | – | – | 3.1 |

| 33 | VMware | United States | technology | not inversion | 2.9 |

| 34 | Abbott Laboratories | United States | life sciences | not inversion | 2.9 |

| 35 | ABP Food Group | Ireland | – | – | 2.8 |

| 36 | Kingston Technology | United States | technology | not inversion | 2.7 |

| 37 | Greencore | Ireland | – | – | 2.6 |

| 38 | Circle K Ireland | Ireland | – | – | 2.6 |

| 39 | Tesco Ireland | United Kingdom | food retail | not inversion | 2.6 |

| 40 | McKesson | United States | life sciences | not inversion | 2.6 |

| 41 | Peninsula Petroleum | Ireland | – | – | 2.5 |

| 42 | Glanbia plc | Ireland | – | – | 2.4 |

| 43 | Intel Ireland | United States | technology | not inversion | 2.3 |

| 44 | Gilead Sciences | United States | life sciences | not inversion | 2.3 |

| 45 | Adobe | United States | technology | not inversion | 2.1 |

| 46 | CMC Limited | Ireland | – | – | 2.1 |

| 47 | Ornua Dairy | Ireland | – | – | 2.1 |

| 48 | Baxter | United States | life sciences | not inversion | 2.0 |

| 49 | Paddy Power | Ireland | – | – | 2.0 |

| 50 | ICON Plc | Ireland | – | – | 1.9 |

| Total | 454.4 | ||||

From the above table:

- US–controlled firms are 25 of the top 50 and represent €317.8 billion of the €454.4 billion in total 2017 revenue (or 70%);

- Apple alone is over 26% of the total top 50 revenue and greater than all top 50 Irish companies combined (see leprechaun economics on Apple as one-fifth of Irish GDP);

- UK–controlled firms are 3 of the top 50 and represent €18.9 billion of the €454.4 billion in total 2017 revenue (or 4%); Shire and Experian are pre the UK transformation to a "territorial" model;

- Irish–controlled firms are 22 of the top 50 and represent €117.7 billion of the €454.4 billion in total 2017 revenue (or 26%);

- There are no other firms in the top 50 Irish companies from other jurisdictions.

Irish media

The role of the Irish media in "framing" the debate around the ethical issues of helping global multinational corporations avoid taxes has been noted.[93] In April 2019, academic research found that "Irish respondents exposed to treatments questioning the morality and fairness of Ireland’s facilitation of Apple tax avoidance are more likely to acknowledge the negative impact on Ireland’s EU neighbours".[94]

Timeline

- 1980 – Apple establishes production facilities in Cork, Ireland.

- 1991 – Irish State agreed the first tax deal with Apple Inc (one of the two rulings cited by the EU Commission).

- 2007 – Original 1991 tax agreement is re-negotiated with Irish State (the second ruling cited by the EU Commission).

- 2013 – US Senate subcommittee examines offshore profit shifting and tax avoidance by Apple Inc.[39]

- 2014 – European Commission opens case against Apple Inc. in Ireland.[45]

- 2015 – Apple re-structures its two Irish subsidiaries (creating the leprechaun economics moment).[12]

- 2016 – European Commission release findings announcing Apple has undue tax benefits owed to Ireland (up to end 2014)[1]

- 2016 – Both Apple Inc.[9] and Ireland[56] announce a decision to appeal the ruling.

- 2017 – European Commission asks for details of Apple's 2015 re-structuring in Ireland[16]

- 2018 – Apple pays the €13bn recovery order (no interest penalty yet) to Ireland (subject to appeal).[10]

- 2020 – Apple wins its appeal at the European General Court (ECG).[24]

- 2020 – The EU Commission announce they intend to appeal the ECG's decision at the CJEU.[95]

See also

- Criticism of Apple Inc.

- Corporation tax in the Republic of Ireland

- Ireland as a tax haven

- Modified gross national income replaced Irish GDP/GNP

- Green jersey agenda

- Feargal O'Rourke architect of Ireland's BEPS tools

- Matheson (law firm) Ireland's largest US tax advisor

- Qualifying investor alternative investment fund (QIAIF) Irish tax-free vehicles

- Single malt arrangement IP-based BEPS tool

- Section 110 SPV Debt-based BEPS tool

- Conduit and Sink OFCs analysis of tax havens

- Panama as a tax haven

- United States as a tax haven

- James R. Hines Jr., leader in academic research on tax havens

- Dhammika Dharmapala, leader in academic research on tax havens

- Gabriel Zucman, leader in academic research on tax havens

Notes

- 2014 Irish GDP was Euro 195.3 billion; see Irish GDP (2009–2017).

- Revealed when the EU Commission published its full COMMISSION DECISION (S.A 38373), page 42 section 2.5.7 Apple's new corporate structure in Ireland as of 2015.[2]

- The extra €1.3 billion has been reported as being interest, however, interest is not payable when there is an appeal; it is more likely that €14.3 billion is the final total fine, excluding interest, as a result of the final audited ASI accounts for 2013 and 2014 being filed.[5]

References

- "European Commission – PRESS RELEASES – Press release – State aid: Ireland gave illegal tax benefits to Apple worth up to €13 billion". europa.eu. 30 August 2016. Retrieved 14 November 2016.

- "COMMISSION DECISION of 30.8.2016 on STATE AID SA. 38373 (2014/C) (ex 2014/NN) (ex 2014/CP) implemented by Ireland to Apple" (PDF). EU Commission. 30 August 2016.

Brussels. 30.8.2016 C(2016) 5605 final. Total Pages (130)

- Foroohar, Rana (30 August 2016). "Apple vs. the E.U. Is the Biggest Tax Battle in History". TIME.com. Retrieved 14 November 2016.

- "Dáil Apple debate: Government wins appeal motion by 93 to 36 votes". The Irish Times. 7 September 2016.

- Seamus Coffey, Irish Fiscal Advisory Council (21 March 2016). "Apple Sales International–By the numbers". Economic Incentives, University College Cork.

- Joe Brennan (30 August 2016). "Revenue insists it collected all taxes Apple owed". Irish Times.

The Revenue Commissioners has insisted it always collected the full amount of tax due from Apple in accordance with Irish law.

- "30 August 2016: Revenue statement on EU commission decision on State aid investigation". Revenue Commissioners. 30 August 2016.

- Halpin, Padraic; Humphries, Conor (2 September 2016). "Ireland to join Apple in fight against EU tax ruling". Reuters. Retrieved 14 November 2016.

- Cook, Tim (30 August 2016). "Customer Letter". Apple (Ireland). Apple Inc. Retrieved 14 November 2016.

- "Apple says it has paid two-thirds of its tax bill". Reuters. 2 August 2016.

- Taylor, Cliff (2 September 2016). "Apple's Irish company structure key to EU tax finding". The Irish Times. Retrieved 14 November 2016.

- Seamus Coffey, Irish Fiscal Advisory Council (24 January 2018). "What Apple did next". Economic Incentives, University College Cork.

- Barrera, Rita; Bustamante, Jessica (2 August 2017). "The Rotten Apple: Tax Avoidance in Ireland". The International Trade Journal. 32: 150–161. doi:10.1080/08853908.2017.1356250.

- "CASE SA.38373: STATE AID TO APPLE". EU Commission. 30 November 2016.

- "Tax Avoidance and the Irish Balance of Payments". Council on Foreign Relations. 25 April 2018.

- O'Dwyer, Peter (8 November 2017). "EU asks for more details of Apple's tax affairs". The Times.

- "Why €13bn Apple tax payment may not be the end of the story". The Sunday Business Post. 28 January 2018.

- "Ireland is the world's biggest corporate 'tax haven', say academics". Irish Times. 13 June 2018.

New Gabriel Zucman study claims State shelters more multinational profits than the entire Caribbean

- "Irish appeal of Apple ruling a 'strange decision', says Moscovici". Irish Times. 9 September 2016.

- "An Analysis of 2015 Corporation Tax Returns and 2016 Payments" (PDF). Revenue Commissioners. April 2017.

- "IDA Ireland Competitiveness". IDA Ireland. March 2018.

- "IRELAND Trade and Statistical Note 2017" (PDF). OECD. 2017. pp. 2–5.

- "Denouncing Ireland as a tax haven is as dated as calling it homophobic because of our past". Irish Independent. 21 June 2018.

The total value of US business investment in Ireland – ranging from data centres to the world's most advanced manufacturing facilities – stands at $387bn (€334bn) – this is more than the combined US investment in South America, Africa and the Middle East, and more than the BRIC countries combined.

- Brennan, Joe (15 July 2020). "Ireland wins appeal in €13bn Apple tax case". Irish Times. Retrieved 15 July 2020.

- https://ec.europa.eu/commission/presscorner/detail/en/STATEMENT_20_1746. Retrieved 18 December 2020. Missing or empty

|title=(help) - "When Steve Jobs and Apple first came to Ireland". IrishCentral.com. 17 January 2012. Retrieved 14 November 2016.

- Leswing, Kif (30 August 2016). "Apple defended its Irish tax-minimizing operation using a classic photo of Steve Jobs in Cork". Business Insider. Retrieved 14 November 2016.

- Cook, James (30 August 2016). "A deal made in 1991 paved the way for Apple's current tax issue". Business Insider. Retrieved 14 November 2016.

- "Interview extracts between Apple tax advisers and Irish Revenue". www.ft.com. Retrieved 14 November 2016.

- "The Guardian view on tax and Ireland: Apple, pay your way". The Guardian. 30 August 2016.

- "Revealed Eight facts you may not know about the Apple Irish plant". 15 December 2017.

- "Apple's multi-billion dollar, low-tax profit hub: Knocknaheeny, Ireland". The Guardian. 29 May 2013.

- Hayes, Terry (2 September 2016). "Apple's €13 billion Irish back-tax bill reverberates around the world – Apple and Ireland to appeal; U.S. denounces decision". Thomson Reuters Tax & Accounting. Retrieved 14 November 2016.

- "Apple Sales International: Private Company Information – Businessweek". www.bloomberg.com. Retrieved 14 November 2016.

- Sheppard, Lee A. (3 June 2013). "Apple's Tax Magic (Apple Inc.'s Tax Planning)". Tax Notes International. 70 (10).

- Harrison, David (December 2014). "Apple's Irish Problem". Accountancy Live. 153.

- "Why there are no Apple Stores in the Republic and probably won't be for a while". thejournal.ie. 15 March 2015.

- O'Brien, Justine Mccarthy Stephen (14 November 2016). "BERTIE AHERN: Revenue 'kept Apple tax deal from cabinet'". Sunday Times.

- "Majority Media | Media | Homeland Security & Governmental Affairs Committee". www.hsgac.senate.gov. Retrieved 14 November 2016.

- Worstall, Tim (21 May 2013). "Apple's Profit Shifting Claims: We're in Humpty Dumpty Territory Here". Forbes. Retrieved 14 November 2016.

- "US Senator repeats Irish 'tax haven' claim". RTÉ.ie. 31 May 2013. Retrieved 14 November 2016.

- Senator Carl Levin; Senator John McCain (21 May 2013). "Offshore Profit Shifting and the U.S. Tax Code – Part 2 (Apple Inc.)". US Senate. p. 3.

A number of studies show that multinational corporations are moving "mobile" income out of the United States into low or no tax jurisdictions, including tax havens such as Ireland, Bermuda, and the Cayman Islands.

- "Senators insists Ireland IS a tax haven, despite ambassador's letter: Carl Levin and John McCain have dismissed the Irish ambassador's account of Ireland's corporate tax system". thejournal.ie. 31 May 2013.

Senators LEVIN and McCAIN: Most reasonable people would agree that negotiating special tax arrangements that allow companies to pay little or no income tax meets a common-sense definition of a tax haven.

- "Ireland rejects U.S. senator claims as tax spat rumbles on". Reuters. 31 May 2013.

- "Commission investigates transfer pricing arrangements on corporate taxation of Apple (Ireland) Starbucks (Netherlands) and Fiat Finance and Trade (Luxembourg)". EU Commission. 11 June 2004.

- Sebag, Gaspard; Doyle, Dara; Webb, Alex (16 December 2016). "The Inside Story of Apple's $14 Billion Tax Bill". Bloomberg News. Retrieved 27 December 2020. Cite magazine requires

|magazine=(help) - "European Commission – PRESS RELEASES – Press release – State aid: Commission investigates transfer pricing arrangements on corporate taxation of Apple (Ireland) Starbucks (Netherlands) and Fiat Finance and Trade (Luxembourg)". europa.eu. 11 June 2014. Retrieved 14 November 2016.

- "CONSOLIDATED VERSION OF THE TREATY ON THE FUNCTIONING OF THE EUROPEAN UNION". eur-lex.europa.eu. Retrieved 14 November 2016.

- "State aid SA.38373 (2014/C) (ex 2014/NN) — Alleged aid to Apple". eur-lex.europa.eu. Retrieved 14 November 2016.

- "Apple ruling is aimed at harming Irish tax regime, claims Noonan". Irish Times. 2 September 2016.

I do. I think they are establishing a bridgehead. There is a lot of envy across Europe about how successful we are in putting the HQ of so many companies into Ireland and especially into Dublin

- "What is state aid? European Commission". ec.europa.eu. Retrieved 14 November 2016.

- "Enda Kenny: Europe trying to bully Ireland with Apple tax ruling". Irish Examiner. 4 September 2016.

- "Taoiseach makes 'no apology' for defending right to appeal EC decision". RTÉ.ie. 3 September 2016.

- "European Commission – Announcement Ireland granted undue tax benefits to Apple". EU Commission. 30 August 2016.

- Byrne, David (30 August 2016). "Minister Noonan disagrees profoundly with the Commission on Apple". An Roinn Airgeadais, Department of Finance. Retrieved 14 November 2016.

- Hannon, Paul (7 September 2016). "Irish Lawmakers Back Appeal on Apple Ruling". Wall Street Journal. ISSN 0099-9660. Retrieved 14 November 2016.

- "Dail backs plan to appeal Apple ruling". RTÉ.ie. 7 September 2016.

Following a lengthy debate in the recalled Dáil, the vote was passed by 93 votes to 36. A number of amendments to the motion were rejected. A Sinn Féin motion calling for the Government not to appeal the ruling was defeated by 104 votes to 28

- "Apple Appeal Against EU Tax Bill Would Enter Uncharted Territory". Fortune. 2 September 2016. Retrieved 14 November 2016.

- "Action brought on 9 November 2016 – Ireland v Commission". CURIA. Retrieved 27 February 2018.

- O'Dwyer, Peter (6 August 2016). "Appeal over Apple tax may start this year". The Times.

State's case gets priority but could last five years

- Louise Kelly (18 September 2018). "State collects €13bn Apple tax bill – plus interest". Irish Independent.

- Rónán Duffy (18 September 2018). "Apple pays over the €14.3bn due to Ireland – but the minister again denies that it's owed". TheJournal.ie.

- Ciara O'Brian (8 October 2018). "Commission drops legal action against Ireland over Apple 'aid'". Irish Times.

The action was taken following a delay of several months in recovering the money from the tech giant. The commission had given Ireland a deadline of 3 January 2017 to reclaim the €13 billion; it referred Ireland to the European Court of Justice on 4 October for failing to comply.

- John Mulligan (31 May 2019). "Apple tax case cost to State is €7m and rising". Irish Independent. Retrieved 31 May 2019.

- Conor McMorrow (30 May 2019). "State's appeal of EU Apple tax ruling has cost €7.1m so far". Retrieved 31 May 2019.

- "ECLI:EU:T:2020:338".

- Carroll, Rory (25 September 2020). "European commission to appeal against €13bn Apple tax ruling". The Guardian. Retrieved 27 December 2020. Cite magazine requires

|magazine=(help) - "Chairman, Fiscal Advisory Council: 'There's been a very strong recovery – we are now living within our means'". Irish Independent. 18 January 2018.

- "Minister Donohoe publishes Review of Ireland's Corporation Tax Code". Department of Finance. 21 September 2017.

- Seamus Coffey Irish Fiscal Advisory Council (30 June 2017). "REVIEW OF IRELAND'S CORPORATION TAX CODE, PRESENTED TO THE MINISTER FOR FINANCE AND PUBLIC EXPENDITURE AND REFORM" (PDF). Department of Finance (Ireland).

- "Capital allowances for intangible assets". Irish Revenue. 15 September 2017.

- "Intangible Assets Scheme under Section 291A Taxes Consolidation Act 1997" (PDF). Irish Revenue. 2010.

- "Capital Allowances for Intangible Assets under section 291A of the Taxes Consolidation Act 1997 (Part 9 / Chapter2)" (PDF). Irish Revenue. February 2018.

- Jesse Drucker; Simon Bowers (6 November 2017). "After a Tax Crackdown, Apple Found a New Shelter for Its Profits". New York Times.

- "BBC Panorama Special Paradise Papers Apple Secret Bolthole Revealed". BBC News. 6 November 2017.

- "Apple used Jersey for new tax haven after Ireland crackdown, Paradise Papers reveal". Independent. 6 November 2017.

- "Apple's Exports Aren't Missing: They Are in Ireland". Council on Foreign Relations. 30 October 2017.

- "Apple tax bill could climb by €9bn as firms dig in". New York Times. 28 January 2018.

- "Apple could owe billions more in tax due to its restructured tax arrangements since 2015 – Pearse Doherty TD". Sinn Féin. 25 January 2018.

- "Tax break for IP transfers is cut to 80pc". Irish Independent. 11 October 2017.

- "Change in tax treatment of intellectual property and subsequent and reversal hard to fathom". Irish Times. 8 November 2017.

- "Carthy questions Vestager on Apple's new tax arrangements". Sinn Féin. 19 February 2019. Retrieved 26 February 2019.

- Seamus Coffey, Irish Fiscal Advisory Council (18 June 2018). "Who shifts profits to Ireland". Economic Incentives, University College Cork.

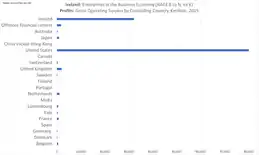

Eurostat’s structural business statistics give a range of measures of the business economy broken down by the controlling country of the enterprises. Here is the Gross Operating Surplus generated in Ireland in 2015 for the countries with figures reported by Eurostat.

- "EU debunks claims about how Ireland can use €13bn Apple tax windfall". Silicon Republic. 31 August 2017.

- "Fianna Fáil to vote for appeal on Apple tax ruling". Irish Times. 6 September 2016.

- James R. Hines Jr.; Anna Gumpert; Monika Schnitzer (2016). "Multinational Firms and Tax Havens". The Review of Economics and Statistics. 98 (4): 714.

Germany taxes only 5% of the active foreign business profits of its resident corporations. [..] Similarly, Irish multinationals do not benefit from this system as the Revenue Commissioners tax Irish Companies on worldwide income, whereas the IRS only tax profits repatriated to the USA. Furthermore, German firms do not have incentives to structure their foreign operations in ways that avoid repatriating income. Therefore, the tax incentives for German firms to establish tax haven affiliates are likely to differ from those of US firms and bear strong similarities to those of other G-7 and OECD firms.

- "Winning FDI 2015–2019 Strategy". IDA Ireland. March 2015.

- "FactCheck: How much do multinationals actually contribute in taxes?". thejournal.ie. 9 September 2016.

- "CRISIS RECOVERY IN A COUNTRY WITH A HIGH PRESENCE OF FOREIGN OWNED COMPANIES: Ireland" (PDF). IMK Institute Berlin. January 2017.

- "Ireland's Top 1000 Companies". Irish Times. 2018.

- Country in which executive decisions are made and main executives live, as opposed to country of legal incorporation

- "Tracking Tax Runaways". Bloomberg News. 1 March 2017.

- Eithne Shortall (21 April 2019). "UCD and Trinity study shows media bolsters support for Irish tax haven". The Times. Retrieved 25 April 2019.

The research states that while public support in post-recession Ireland could be expected to turn against "the facilitation of low corporate taxes" for multinational companies such as Apple, this was not the case.

- Prof. Aidan Regan; Prof. Liam Kneafsey (19 April 2019). "The Role of the Media in Shaping Attitudes Toward Corporate Tax Avoidance: Experimental Evidence from Ireland" (PDF). University College Dublin. Retrieved 25 April 2019.

- https://ec.europa.eu/commission/presscorner/detail/en/STATEMENT_20_1746. Retrieved 18 December 2020. Missing or empty

|title=(help)